While the U.S. tax system appears to be federal in nature, the U.S. uses the Internal Revenue Code to cast a wide web and bring international persons and entities under its taxing power. Not only does this web capture foreign persons physically present in the U.S. but it also captures foreign companies statutorily deemed as being controlled by U.S. Shareholders; in the tax world, these companies are called controlled foreign companies, or CFCs. The Code focuses on a few highly complex provisions on tax laws applicable only to CFCs and their shareholders, and failure to comply with them is likely to result in high punishments, both civil and criminal. Thus, it is critical that you, whether you own a foreign company or have a client who owns a foreign company (either directly, indirectly, or constructively), understand if that company will be classified as a CFC under the Code.

What Is a Controlled Foreign Corporation (CFC)?

A foreign corporation will be classified as a CFC if more than 50% of the total combined voting power of all classes of stock is owned directly, indirectly, or constructively, by a U.S shareholder on any day during the taxable year.

Controlled Foreign Corporation Examples

John is a U.S. person who owns 100% of Foreign Company A (A). Due to John owning more than 50% and at least 10% A will be a CFC.

John (same as above) owns 51% of Foreign Company B (B). Due to John owning more than 50% and at least 10% B will be a CFC.

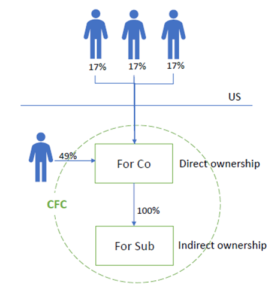

John owns 11% of Foreign Company C (C), Peter and his wife who are both U.S. persons, own 20% each of C. C will therefore be a CFC as it exceeds the 50% threshold.

John owns 49% in Foreign company D and the only U.S. shareholder. An exemption applicable to John and the CFC rules can’t apply.

Controlled Foreign Corporation Fundamentals

CFC rules aren’t unique to the US. Many countries around the world have CFC legislation. The CFC rules were developed by the IRS in order to prevent taxpayers from hiding their money in foreign businesses and therefore have a lower tax rate. Section 957 defines the rules and who may be subject to tax.

How Does a Controlled Foreign Corporation Work?

Only non-US companies that are classified as corporations by the Internal Revenue Services can be regarded as CFCs.

Typically, shareholders pay taxes on the income of the corporation only when they take dividends. If a shareholder of a US domestic corporation takes dividends, they must be reported each year, using form 1099-DIV. However, should these taxpayers take dividends or other forms of income from a foreign corporation, they assume they don’t have to report that income or pay taxes on it. And this is where the CFC rules come into play as a way to charge taxpayers on their income from foreign corporations.

Motivations

The tax law in many countries, including the US, does not normally tax a shareholder of a corporation on the corporation’s income until the income is distributed as a dividend.

The CFC rules of Subpart F, and later of other countries’ tax laws, were intended to cause current taxation to the shareholder where income was of a sort that could be artificially shifted or was made available to the shareholder. At the same time, such rules were intended not to interfere with active business income or transactions with unrelated parties.

What is Attribution and Constructive Ownership?

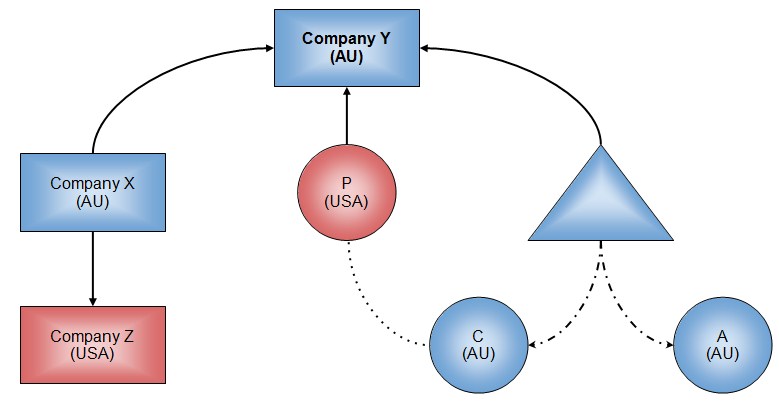

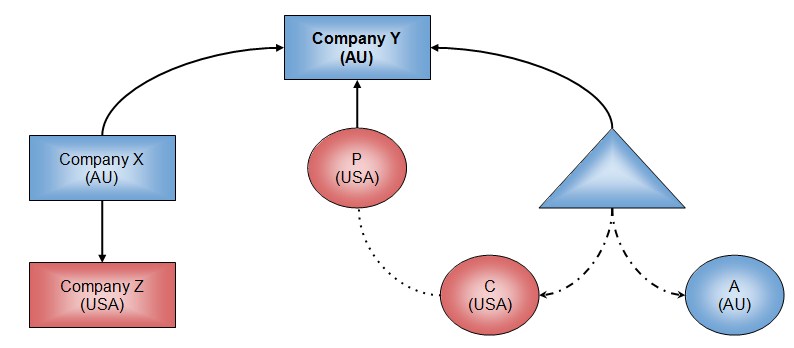

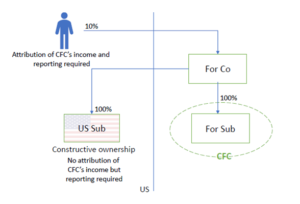

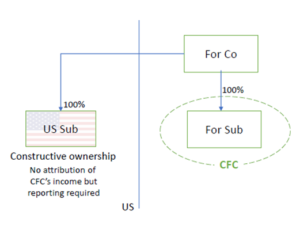

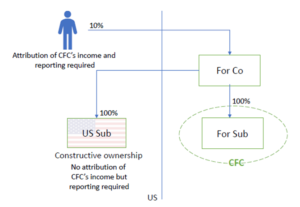

The Tax Cuts and Jobs Act (TCJA) was enacted in December 2017 and changed a constructive ownership rule that determines whether a foreign corporation is a CFC for federal income tax purposes.

With the new law, a U.S. corporation, U.S. partnership, or U.S. trust in which a foreign taxpayer is a shareholder, partner, or beneficiary is now considered to own the stock in a foreign entity that the foreign person owns directly. The foreign person must own more than 50% of the U.S. corporation before the U.S. corporation is considered to own the foreign corporation’s stock.

Basic Mechanisms

The basic mechanisms of CFC rules are that a U.S. person who is regarded as a U.S. shareholder of a CFC must include in their income that person’s share of the CFC’s income. The includible income generally includes income received by the CFC…

- From investment or passive sources, including:

- Interest and dividends from unrelated parties,

- Rents from unrelated parties, and

- Royalties from unrelated parties;

- From purchasing goods from related parties or selling goods to related parties where the goods are both produced and for use outside the CFC’s country;

- From performing services outside the CFC’s country for related parties;

- From non-operating, insubstantial, or passive businesses, or of a similar nature through lower-tier partnerships and/or corporations.

Firstly, the rules contain an ownership threshold to determine if a foreign entity is sufficiently controlled by domestic shareholders to be considered a CFC.

Secondly, there is a taxation condition that can include a rule to determine whether the income of the CFC has already been taxed at a minimum level by the foreign country.

Thirdly, CFC rules identify the type of income to which the rules are applicable, whether only passive income (that is, interest or capital gains) or all income that is received by the CFC.

U.S. Code: Controlled Foreign Corporations

General Rule

The general rule regarding Controlled Foreign Corporations can be found in the Internal Revenue Code §957(a)(1-2)

“For purposes of this title, the term “controlled foreign corporation” means any foreign corporation if more than 50 percent of—

(1) the total combined voting power of all classes of stock of such corporation entitled to vote, or

(2) the total value of the stock of such corporation, is owned (within the meaning of section 958(a)),or is considered as owned by applying the rules of ownership of section 958(b), by United States shareholders on any day during the taxable year of such foreign corporation.”

Special Rule for Insurance

IRC §957(b) includes a special rule for insurance.

“For purposes only of taking into account income described in section 953(a) (relating to insurance income), the term “controlled foreign corporation” includes not only a foreign corporation as defined by subsection (a) but also one of which more than 25 percent of the total combined voting power of all classes of stock (or more than 25 percent of the total value of stock) is owned (within the meaning of section 958(a)), or is considered as owned by applying the rules of ownership of section 958(b), by United States shareholders on any day during the taxable year of such corporation, if the gross amount of premiums or other consideration in respect of the reinsurance or the issuing of insurance or annuity contracts not described in section 953(e)(2) exceeds 75 percent of the gross amount of all premiums or other consideration in respect of all risks.”

United States Person

IRC §957(c) stipulates the following –

“For purposes of this subpart, the term “United States person” has the meaning assigned to it by section 7701(a)(30) with certain exceptions applicable.”

Asena advisors. We protect Wealth.

Purpose

The purpose of the CFC regime is to reduce and eliminate the deferral of certain CFC income. With the CFC regime, the IRS has authority over U.S. shareholders to prevent the deferral of tax.

Avoiding CFC Status

For federal income tax purposes, a foreign entity may be classified as a corporation or flow-through entity. In terms of the check-the-box rules, shareholders may be able to elect to treat their shares of gross income, deductions, and taxes of a foreign corporation as earned and paid by themselves (i.e. as a flow-through). This enables the U.S shareholders to obtain credits for foreign taxes paid by the entities they own, which credits might otherwise not be available.

Special Considerations

U.S. shareholders of CFCs are subject to specific anti-deferral rules under the U.S. tax code, which may require a U.S. shareholder of a CFC to report and pay U.S. tax on undistributed earnings of the foreign corporation.

U.S. shareholders with controlling interests in foreign corporations must report their share of income from a CFC and their share of earnings and profits of that CFC, which are invested in United States property.

The CFC tax rules in accordance with Subpart F allow the IRS to tax certain income of the CFC, even though the corporation is foreign, and the U.S. would have no direct authority over the foreign corporation.

If there is current year earnings and profit, a U.S. shareholder may be subject to tax on his share of income, whether distributed or not.

The CFC tax rules are extremely complex. The introduction of the new international tax rules referred to as Global Intangible Low-Taxed Income (GILTI) just added to the complexity.

Even though GILTI is not the same as Subpart F income, it is equally complex.

Who is a U.S. Shareholder?

The IRS stipulates that:

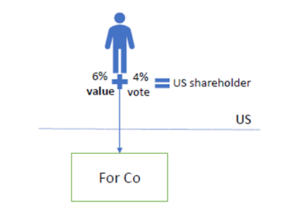

“A U.S. shareholder is a U.S. person (defined in IRC 957(c)) who owns directly, indirectly, or constructively 10 percent or more of the total combined voting power of stock entitled to vote or 10 percent or more of the total value of all classes of stock entitled to vote in a foreign corporation. Internal Revenue Code 958(a) provides rules for determining direct and indirect stock ownership of a corporation.”

How are CFCs Reported?

The CFC must file an annual report on IRS Form 5471, “Information Return of U.S. Persons With Respect to Certain Foreign Corporations.” This form is completed and attached to the corporation’s income tax return.

Controlled Foreign Corporation Penalties for Not Reporting

The penalties for not properly reporting these forms can be brutal. But, the Internal Revenue Service has developed various offshore voluntary disclosure programs such as the streamline program, delinquency procedures, and Post-OVDP to assist you.

Common Controlled Foreign Corporation FAQs

What is IRC Section 957?

It’s the section of the internal revenue code dealing with the general rule of what is a CFC and a U.S. person.

What is CFC IRS?

CFC IRS is just an abbreviation for Controlled Foreign Corporations (CFC) and Internal Revenue Services (IRS).

Foreign Corporation Tax Reform

With the introduction of TCJA, GILTI, and updated Form 5471 reporting requirements, the landscape for reporting Controlled Foreign Corporations has intensified.

Dividends

Dividends are generally taxed in the year they are received. In addition, there may be some Subpart F income for the controlled foreign corporation — even in years when no income was distributed.

More Than 50% U.S. Ownership

In order for a Foreign Corporation to be considered a Controlled Foreign Corporation, it must be owned more than 50% by U.S. Persons.

10% Ownership

Secondary to the 50% requirement, it must also be that each of the U.S. shareholders within that +50% each own at least a 10% share.

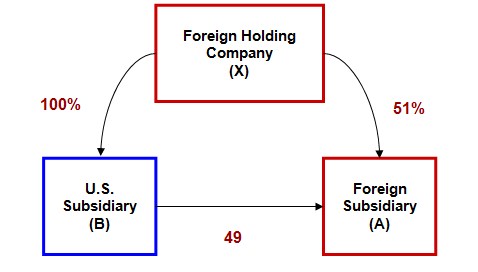

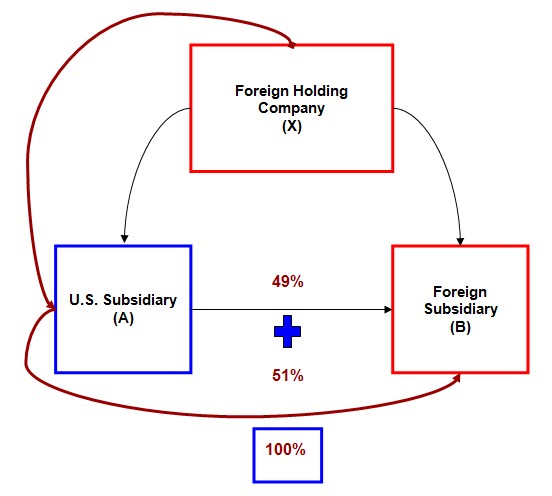

What is Attribution IRC (958)?

Attribution is the idea that one person is considered to constructively own stock that another person owns – only due to the relationship between the two individuals. The main purpose of attribution is to avoid artificially low tax reductions strategies by making sales or transfers between “related” parties.

What is Subpart F Income (IRC 951)

It is income that is earned within a Controlled Foreign Corporation that is going to be taxed to the U.S. person, irrespective of being distributed to the U.S. person.

But I Did Not Receive any Subpart F Income Distribution?

It is irrelevant whether the U.S. shareholder of a CFC received any of the money.

There are certain other factors that are important regarding subpart F income such as whether there is any current earnings and profits (E&P), whether taxes have been paid, and whether dividends have also been issued.

What is Form 8938?

Form 8938 (Statement of Specified Foreign Financial Assets) is an IRS Form associated with Foreign Account Tax Compliance Act (FATCA). The IRS has made Foreign Financial Reporting a key enforcement priority.

The failure to file this FATCA Form can lead to extensive Fines and Penalties.

CFC Penalties Will Flow Through 8938

There are many penalties a person may be subject to if they have a controlled foreign corporation but did not file properly. These include penalties for not filing an FBAR or 8938.

The Form 8938 Penalties range from a warning letter, all the way up to +$50,000. This does not include other potential penalties, such as FBAR Penalties.

You may be subject to penalties if you fail to timely file a correct Form 8938 or if you have an understatement of tax relating to an undisclosed specified foreign financial asset.

If you are required to file Form 8938 but do not file a complete and correct Form 8938 by the due date (including extensions), you may be subject to a penalty of $10,000.

The maximum additional penalty for a continuing failure to file Form 8938 is $50,000.

For more information on CFCs, please contact one of our specialists at Asena Advisors. We make sure that your specific needs are catered for.

Shaun Eastman

Peter heads Asena Advisors in North America and a member of the global executive of Asena International. Janpriya is the head of the US-India practice and US Operations Head with Asena Advisors.They can be reached directly at

Peter heads Asena Advisors in North America and a member of the global executive of Asena International. Janpriya is the head of the US-India practice and US Operations Head with Asena Advisors.They can be reached directly at  Initial analysis that we have undertaken for our clients has shown that the Tax Reforms can result in burdensome and costly compliance requirements even in situations where no further tax may be due. Careful and diligent planning should be undertaken with respect to the Tax Reforms when addressing international tax planning for foreign business owners and investors to avoid unintended and costly results. Foreign investors who are in the process of exploring US markets should be vigilant of the possible tax exposures that can impact their global business.

Initial analysis that we have undertaken for our clients has shown that the Tax Reforms can result in burdensome and costly compliance requirements even in situations where no further tax may be due. Careful and diligent planning should be undertaken with respect to the Tax Reforms when addressing international tax planning for foreign business owners and investors to avoid unintended and costly results. Foreign investors who are in the process of exploring US markets should be vigilant of the possible tax exposures that can impact their global business.

The Tax Reforms are promoted as atransition from worldwide taxation to territorial taxation system for domestic corporations. These reforms are effectively capturing the income of foreign corporations classified as CFCs under different baskets, namely GILTI and transition tax in addition to what was already included as Subpart F income. For large US and foreign corporations, BEAT adds to an already burdensome tax cost for doing business in the US. With this approach, scrutinizing foreign corporations under downward attribution CFC rules will be dissuading US subsidiaries in foreign business structures.

The Tax Reforms are promoted as atransition from worldwide taxation to territorial taxation system for domestic corporations. These reforms are effectively capturing the income of foreign corporations classified as CFCs under different baskets, namely GILTI and transition tax in addition to what was already included as Subpart F income. For large US and foreign corporations, BEAT adds to an already burdensome tax cost for doing business in the US. With this approach, scrutinizing foreign corporations under downward attribution CFC rules will be dissuading US subsidiaries in foreign business structures.