LLC Australia

With ties and clients in Australia, we here at Asena Family Office often get questions about how to set up an LLC there, including if there are differences that one should know about between Australia and the U.S. Today, we will be going over what an Australian LLC looks like, operates, and the people behind it.

What does LLC Company mean?

In the U.S., you can set up an LLC, which is short for a Limited Liability Company. However, in Australia, it is a company that is primarily called either a Proprietary Limited Company or a Private Proprietary Company.

What is Limited Liability Company in Simple Words?

It is the Australian equivalent of a US LLC, a Proprietary Limited Company, or a Private Proprietary Company.

What are the Characteristics of an LLC in Australia

Some of the most essential requirements for both public and private limited companies in Australia are:

-

- Shares – Private companies can privately issue shares, while public companies can offer their shares to the public if the company operates as a listed company;

- Directors – Public companies must have three or more company directors, and two must be Australian residents, while private companies must have one or more directors who are Australian residents;

- Corporate meetings – Also known as annual meetings;

- Taxes – The rates for two corporate incomes are considered applicable as 30% and 27.5% for small companies, but beginning in 2021, the reduced corporate tax has been charged at a lower rate.

Why Would A Company Be An LLC?

Australia does not have a check-the-box regime (CTB rules) as the U.S. does.

For Australian purposes, an LLC is incorporated as per the Corporations Act; investors can incorporate a private or a public company when the company first goes into operation. There is no separate definition or election for tax purposes in Australia.

Is An LLC The Same As A Company?

It is similar to a US LLC to limit the business owner’s risks. However, for Australian purposes, it is a Company called either a Proprietary Limited Company or a Private Proprietary Company in Australia.

Can An LLC Be A Private Company?

Absolutely. With various options, please speak with one of our advisors about which option will be the best for you.

What is the Difference Between LLC and LTD Company?

To simply put, there is no difference. An LTD Company is a type of LLC, and when registering an LLC in Australia, it is registered as a company. On the other hand, an LTD Company is a type of LLC in Australia, which is a public limited company, and shares are open to the public.

What is an S Corporation in Australia?

Australia does not have the option to elect your company as an S Corporation as the U.S. does for federal tax purposes. There are no CTB regimes in Australia as there are in the U.S.

What is the Difference between PTY LTD and LTD?

Some key points to note when understanding the differences between these two forms of company are:

- Shares – a private company can privately issue shares, while a public company can provide its shares to the public if the company decides to operate as a listed company; and

- Directors – the public company is required to have at least three, preferably more, company directors, with two required to be Australian residents. Meanwhile, the private company must preferably have one or more directors who are also residents;

Is PTY LTD a Limited Liability Company?

Yes. A Limited Liability Company is often incorporated according to the Corporations Act, and when registering the company, investors can either incorporate a private or a public company.

What is a PTY LTD Company in Australia?

Pty Ltd is a Private Limited Liability Company and is the most common company used by business owners in Australia. It is often considered restricted by current and future entrepreneurs as it is not allowed to have more than 50 non-employee shareholders. A Pty Ltd is also limited by one or more shares, as it is usually incorporated along with a share capital that is made up of shares claimed by each initial member upon the company’s incorporation. Members are also legally liable only to the point of any unpaid amounts that are on their shares. That is, their personal assets are not at risk in the event of the company being wound up. And it’s prohibited from offering shares to anyone other than existing company shareholders, employees, or a subsidiary company.

Why Do Companies Have PTY LTD?

A proprietary company with a limited liability decreases the risks of doing business because it is regarded as wholly independent from the company’s founders and members, and liability limits its share capital.

Asena advisors. We protect Wealth.

Can You Make An LLC in Australia?

The short and direct answer is yes. A Limited Liability Company is to be incorporated according to and under the Corporations Act. When first starting the company, investors can include private or public companies. There is no need to subscribe to a minimum paid-up company for either business form. However, there are specific provisions: the public company cannot have a maximum number of specified shareholders. However, the private one must have a maximum of fifty shareholders who are under employment within the company. For both Australian LLCs, the minimum number of shareholders is one.

What Is A Limited Liability Company Australia?

It is a company that is incorporated in terms of the Corporations Act 2001, and when first opening the company, investors can either incorporate a private or a public company.

What are the Basic Steps for Company Incorporation in Australia?

Typically, your first step to forming an Australian company is choosing your business type. Suppose you’ve decided to start a Proprietary Limited Company (LLC) in Australia. In that case, the next steps are as follows:

- Reserve your company and/or business name;

- Appointing a Company Director and other statutory officeholders;

- Drafting and signing any bylaws for your LLC in Australia;

- Registering your Proprietary Limited Company (LLC) in Australia;

- Get your business and tax identification numbers and

- Open a corporate bank account.

What Are The Bylaws of an Australian Limited Liability Company?

There’s more than one way to choose the kind of governance of your Australian Proprietary Limited Company (LLC) will have. To do this, you can choose to either:

- Operate your company under the replaceable rules that are listed under the Corporations Act;

- Create a unique constitution or incorporate elements from the replaceable rules and include your own; and

- Appoint a sole director to your Proprietary Limited Company who is also a single shareholder and doesn’t need a formal internal governance system.

Opening an LLC in Australia

Each initial startup steps are unique for every Australian. Below are common courses of action to consider unless there is another that would be the most beneficial for you and the structure of your business.

Requirements for an LLC in Australia

When starting a Proprietary Limited Company or Private Proprietary Company in Australia, the minimum requirements include the following:

-

- Zero minimum share capital;

- One shareholder;

- One company director; and

- One resident director.

Once you have the proceeding, you’ll need to produce annual financial statements. However, you won’t need to register for a GST (Goods and Service Tax) unless your sales exceed A.U. $75,000 in the year.

What Licenses Are Necessary To Open A LLC In Australia

Standard Australian licenses and permits for any business either:

-

- Give approval to your business to do an activity; or

- Protect your business and employees with additional legal security.

Licensing and permit requirements will often vary by local laws, state, and industry; what you’ll need depends on your business type, business activities, and location.

What are the Main Steps in Registering an LLC in Australia?

Once you have selected the LLC type (either the public or the private one), you need to consider conserving a suitable trading name. Just like within other jurisdictions around the world, the Australian company’s trade name that is soon to go onto the market has to be unique nationwide. When deciding on a trading name, verifying if the chosen name has not already been activated or if it is already registered as a trademark in Australia is compulsory. You can always find experts at Asena Family Office for cases concerning intellectual property regulations.

Another critical step is to prepare the company’s statutory documents. It is required that the documents are to be processed through which the legal entity will inherit a legal personality, being a separate entity from its founders. It is also vital to choose directors, followed by registering with the local institutions for tax purposes, per the law’s regulations. Another legal obligation to check off your list is to have an official business address, including your company’s headquarters and the development of its activities. This is a critical step for all companies registered in Australia, not only for LLCs.

One thing to note about LLCs is that they are suitable for most of Australia’s development of economic activities, including importing and exporting raw materials and other goods. Regarding its taxation, investors must know that your company will be liable for all corporate taxes applied under your local tax law and benefits from the treaties signed to avoid double taxation.

An Australian Private Limited Liability Company is not always required to finalize and turn in an audit. When drafting any statutory documents, you will be required to add provisions concerning the internal management rules of the company, its shareholding structure, and the rights and obligations of any parties that are involved with or in the company, such as shareholders and directors.

How Do I Form an LLC in Australia?

I like to recommend the following six checkboxes for clients when beginning the process of starting a Proprietary Limited Company or a Private Proprietary Company.

Reserve Your Company and/or Business Name

Each company in Australia must have its unique company name that does not infringe on another.

If you don’t decide on a company name when forming your Australian LLC, the Australian Company Number (ACN) will be your company name during the formation process.

It is important to note that Business names don’t create new, separate entities, and your business name is your trading name.

Draft and sign bylaws for your LLC in Australia

Following the name selection, you need to make a decision on the governance of your Proprietary Limited Company (Australian LLC). Multiple courses of action are available, as you can choose to:

-

- Operate your company under the replaceable rules that are listed under the Corporations Act;

- Design a unique constitution;

- Add elements of the replaceable rules and include your own; and

- Select a Proprietary Limited Company with a sole director (who also acts a single shareholder) and doesn’t need a formal internal governance system.

Appoint a Company Director and Other Statutory Officeholders

First and foremost, you’ll need to hire on a legal representative currently residing in Australia to create your LLC. Usually, another name for their role in Australian entity formation is the Company Director, with every proprietary company requiring at least one for initial and long-term needs. The reason why is that the Company Director, as the resident legal representative, is responsible for overseeing the affairs of the new local company.

Foreign companies can also appoint a Nominee Director. They are an external legal expert hired onto the company but are authorized, similar to the Company Director, to make legal decisions on its behalf. Both directors are responsible for ensuring the company fully complies with all Corporations Act obligations.

Register your Proprietary Limited Company (LLC) in Australia

It’s possible to register your company either on paper or online, with Australia’s Business Registration Services providing an online portal for application completion if you are unable to be at their office in person.

There are, however, certain cases where a company can’t register online.

Once it is approved, your Proprietary Limited Company will be sent its Australian Company Number (ACN), Australian Business Number, registration certificate, and a corporate key to securely update your company information.

Get Your Business and Tax Identification Numbers

Following your initial registration, you will need to file for the appropriate taxes for your Australian LLC. One example is that every business must have a tax file number (TFN) to start tax filing, which is automatically produced when you obtain your Australian Business Number (also known as ABN for short).

The ABN is a distinctive 11-digit number that is used to identify your business to not only the government but your local community, too. Done on paper at the office, the process can also be completed over the Internet through the Business Registration Service website.

Depending on your circumstances and industry, you may be required by the BRS to register for any goods and services (GST) withholding, income, and fringe benefits taxes.

Open a Corporate Bank Account

Once the above steps are completed and your company has been registered, you can get started on setting up a corporate bank account.

Australia’s Anti-Money Laundering and Counter-Terrorism Financing Act in 2006 has set up rigid regulations for banks to undertake their due diligence with new applicants. For this reason, you can expect to provide a wide range of documentation confirming information, identification, and details of your newly-registered company.

Important Things to Know When Setting Up an LLC in Australia

Your Australian LLC (Proprietary Limited Company or Private Proprietary Company) will need an official business building or office, such as a registered address where it is to have a physical place of business for meetings (most often optional) and receive all official documents.

This is part of the registration process; all Australian LLCs are required to have a physical address that can be used for business purposes and activities. During the registration, all institutions involved with the procedure will be required to provide information and all evidence that confirms where your company’s headquarters will be.

The official business address can be any location that works best for your structure, such as an apartment, an office building, or another type of premises. Your final decision will depend on the needs of the business, such as necessary space and the type of activity carried out, whether administrative or otherwise. One can also build an office if one finds it necessary and more affordable than buying or renting a space.

Asena Advisors focuses on strategic advice that sets us apart from most wealth management businesses. We protect wealth.

How Much Is A Business License In Australia?

It will depend on the type of industry you are categorized in, with some starting at AUD $300.

What are the Registration Costs for a Company in Australia?

The most common cost often ranges from AUD $443 to AUD $538. Your final amount will be dependent on the type of company you register.

How Much Does an LLC Cost in Australia?

Same as above and will be dependent on the type of company and industry.

How Much Does a PTY LTD Cost?

Pty Ltd costs are similar to the typical company numbers for registration. However, there are cases where it can go at a lower number, such as AUD $400 to AUD $500.

Reviewing your thoughts on what we’ve discussed and how it may factor into your company, there are additional base notes to understand Australia’s tax and classification system and expectations before coming to a conclusion.

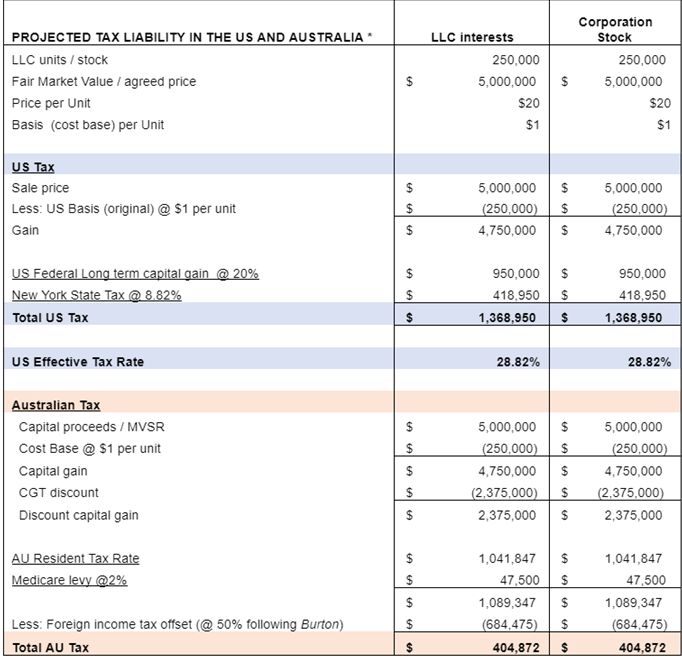

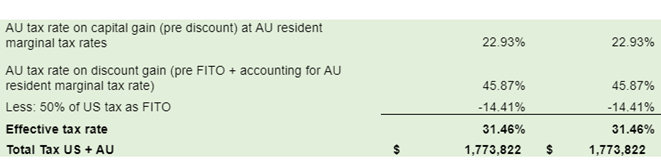

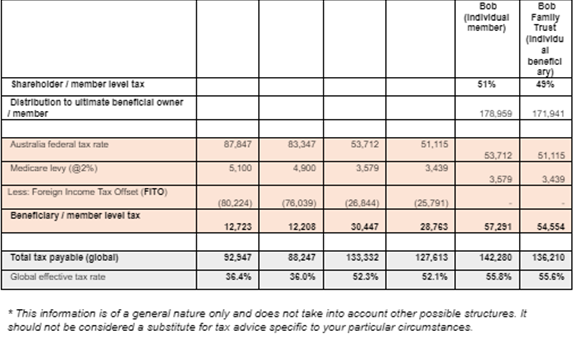

What are the Main Taxes for a Limited Liability Company in Australia

A crucial consideration for companies in Australia is the country’s taxation system that applies to them. Companies often recognized as corporate structures, including an L.L., whether private or public, will be taxed following the Australian corporate tax system.

If the company has an annual turnover that is above AUD $75,000, it is crucial to obtain an Australian Business Number (ABN).

If the company has an income below a certain threshold in a financial year, it will be taxed using a 27.5% corporate tax rate, representing a corporate tax that has been reduced.

However, for the last year (2021 as of this posting), the lower tax rate has been reduced to only 26%. It is predicted to further reduce in the next financial year (2022 as of this posting) to 25%, as according to the Australian Taxation Office, as the standard corporate tax rate charged to Australian companies is 30%. And in 2017-2018, the threshold in which the reduced corporate tax rate had been applied summed up to a total of AUD $25 million. However, beginning in 2018-2019, the threshold increased to a total of AUD $50 million.

Please take into consideration that the Australian financial year is different from the standard financial year in other countries (from 1st January to 31st December). In Australia, the financial year begins on 1st July and ends on 30th June, but companies can decide to follow the worldwide financial period.

Is An LLC Company Good?

An LLC in Australia is a company type suitable for those who want to form a small or medium-sized entity. For those interested in a public limited company, it is vital to find out that the legal entity can be listed on the Stock Exchange.

Contact the Experts to Form Your LLC in Australia

Our experts at Asena Family Office have extensive experience advising entrepreneurs and setting up businesses in Australia that suit their needs. Please do not hesitate to contact us if you require assistance.

Connect with us in the righthand column to learn how to get started on your own LLC in Australia.

Shaun Eastman

Peter Harper