LLC Series: The US and Australian Tax Effect of Holding Membership Interests in an LLC vs Stock in a US Corporation

How should an Australian resident investor hold their interest in a business that has high turnover and potential for significant income distributions? What does the cross border flow of funds look like?

How you structure your business can have a tremendous impact on your ability to access income and capital distributions, your tax reporting and payment obligations (and in a cross-border context, the “global” effective tax rate), regulatory obligations, and how you eventually sell your interest in the business.

An LLC provides a “flow through” structure to the members, with no additional tax disclosure or reporting obligations in the US (if the LLC has not elected to be taxed as a corporation). For Australian tax purposes, income from an LLC is generally treated as partnership income and disclosed accordingly (see our previous blog: LLC Series: LLCs – US and Australia Classification and Tax Considerations).

A US corporation is treated as a separate entity for tax purposes, and is subject to tax at both the entity level, and the stockholder level. There are additional IRS disclosure and reporting obligations both at the entity level and the stockholder level, due to the double layer of corporate taxation. Unlike in Australia, dividends paid to stockholders are not subject to franking credits and are subject to US withholding taxes.

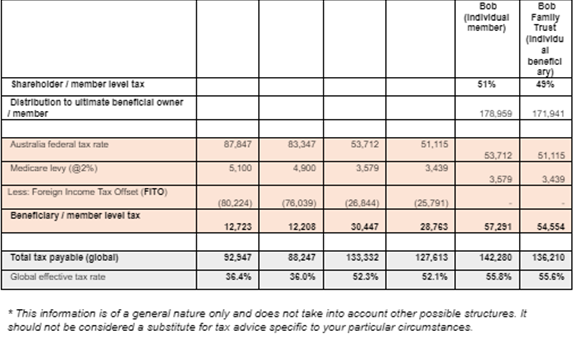

The table below indicates that for an Australian resident individual, it is more tax effective to hold an LLC membership interest personally or through an Australian resident discretionary trust. Holding a C-Corp interest can result in a tax leak due to the double layer of US corporate tax. The most tax inefficient result would be for an Australian resident company to hold a C-Corp interest, with the loss of the foreign income tax offset and the application of Subdivision 768-A resulting in the foreign sourced dividend being non-assessable non-exempt income.

The flow of funds in each scenario could look like this:

Assumptions:

Shareholders are AU Tax residents

$ Values are USD and do not account for FX rates

AU 2020-2021 resident tax rates applied

US Federal and NY State 2020 tax rate applied

For more information, please contact:

Renuka Somers

Head, US-Australia Tax Desk

2025 Australian Federal Budget Summary On Tuesday, March...

In our 13th installment of the Family Office...

2024 Australian Federal Budget Summary On Tuesday 14th...