Restructuring your US operations – Part 2: US corporate reorganization relief

As with the Income Tax Assessments Acts, the Internal Revenue Code (IRC) provides for tax relief (“nonrecognition”) for corporate reorganizations (under sections 354-368).

To qualify for nonrecognition, a restructure must satisfy:

1. one of the statutory definitions of “reorganization”; and

2. other requirements in the Treasury Regulations which restate the judicial tests.

The definition of “reorganization” includes a “scrip for scrip” type restructure – the acquisition by one corporation, in exchange solely for all or a part of its voting stock, stock of another corporation – where immediately after the acquisition, the acquiring corporation has “control” of the other corporation (by possessing at least 80% of the total combined voting power and shares of all classes of stock).

The restructure can involve one or more “domestic corporations” (i.e. if they are created or organized in the United States or under the laws of the United States, or any of its states), a domestic corporation and a “foreign corporation” (i.e. a company registered in Australia).

A LLC would not qualify for corporate reorganization relief and may need to be converted to an Inc. first ( See Restructuring your US operations – Part 1: why, and how you would convert an LLC to an Inc.).

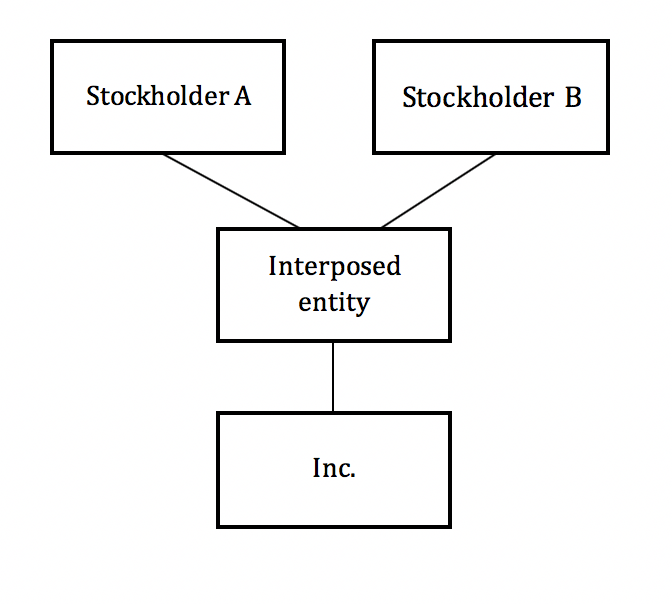

A restructure could therefore look like this, if (for example), it involves the interposition of a new entity:

The Treasury Regulation requirements for a reorganization (included in Reg. 1. 368-1) are:

1. the “continuity of interest” (COI) requirement which stipulates that a substantial part of the value of the proprietary interests in the “target corporation” be preserved though an exchange for an equivalent interest in the “acquiring corporation”;

2. the “continuity of business enterprise” (COBE) requirement which stipulates that a reorganization transaction “must be an ordinary and necessary incident of the conduct of the enterprise and must provide for a continuation of the enterprise. This requirement is broadly satisfied if the issuing corporation continues the target’s historic business or uses a signification portion of the target’s business assets in a business; and

3. the “business purpose” requirement which stipulates that the transaction have a bona fide business purpose, especially where the parties are related and a collateral tax benefit may be obtained from the transaction.

Assuming that these requirements are satisfied, a restructure may be undertaken tax-free, as generally no gain or loss is recognized if stock (or securities) in a corporation that is a “party to a reorganization” is, in pursuance of the “plan of reorganization”, “exchanged solely for stock or securities” in that corporation or in another corporation that is a party to the reorganization. Similarly, no gain or loss is recognized if a corporation is a party to a reorganization and exchanges property, in pursuance of the plan of reorganization, solely for stock or securities in another corporation that is a party to the reorganization.

A “plan of reorganization” requires formal recognition (either written or oral) of the reorganization plan and an identification of the transactions which are treated as part of the reorganization – this can be evidenced through discussions and negotiations. Each party to the reorganization must adopt the plan and file IRS statements for the tax year in which the reorganization occurs.

The “basis” (cost base) of each share of stock received in an exchange to which the reorganization relief applies is generally the same as the basis of the share(s) of stock for which it was exchanged. If a shareholder has different bases in different shares of stock, the basis of each share of stock received in the acquiring corporation will be traced through to the basis of each original share of stock in the target corporation.

If the restructure involves a “foreign corporation” such as an Australian company, the anti-avoidance rules in the IRC require careful review and consideration (see Restructuring your US operations – Part 3: Anti-avoidance rules in the Internal Revenue Code).

The concepts discussed in this blog are complex and require careful consideration to ensure compliance with Australian and US tax laws.

This blog is part of a 3 part series comprising:

Restructuring your US operations – Part 1: why, and how you would convert an LLC to an Inc.

Restructuring your US operations – Part 2: US corporate reorganization relief

Restructuring your US operations – Part 3: Anti-avoidance rules in the Internal Revenue Code

For more information, contact:

Renuka Somers

Senior Tax Advisor

U.S. Australia Tax Desk

2025 Australian Federal Budget Summary On Tuesday, March...

In our 13th installment of the Family Office...

2024 Australian Federal Budget Summary On Tuesday 14th...