LLC Series: The US and Australian Tax Implications of Selling an LLC Interest vs Selling Stock in a US Corporation

How should an Australian resident investor hold their interest in a business that has a high potential for capital growth?

How you structure your business can have a tremendous impact on your ability to access income and capital distributions, your tax reporting and payment obligations (and in a cross-border context, the “global” effective tax rate), regulatory obligations, and how you eventually sell your interest in the business.

What are the tax implications for an Australian resident investor of a sale of an LLC interest vs the sale of stock in an US corporation?

Stock in a US corporation is a capital asset. Similarly, a membership interest in an LLC is usually a capital asset [see LLC Series: Selling or Converting an LLC Interest – the US Tax Implications: Partnerships, “Effectively Connected Income” and the US Non-Recognition Rules].

The US and Australian tax implications of a sale of an LLC interest (classified on capital account) vs stock would usually be the same for an Australian resident individual holding that interest directly, or who receives a distribution of the gain through an Australian resident discretionary trust. However, the structuring of the interest can have an impact on income flow and effective tax rates [this is discussed in our blog LLC Series: The US and Australian Tax Effect of Holding Membership Interests in an LLC vs Stock in a US Corporation]

Structure can also affect the sale price as for US tax purposes, a purchaser acquiring stock in a corporation takes on the double layer of US corporate tax as the corporation is taxed on profits and the stockholders are taxed on dividends (with no US equivalent of the Australian franking credit). Additionally, a purchaser would have a fair market value tax basis in the shares of the corporation (a non-amortizable asset), but not in the assets of the corporation. In contrast, if they were to purchase of an LLC interest, they would be able to obtain a fair market value tax basis in the underlying LLC assets and amortize those assets for tax purposes. Therefore, holding US corporate stock could result in a discounting of a future sale price.

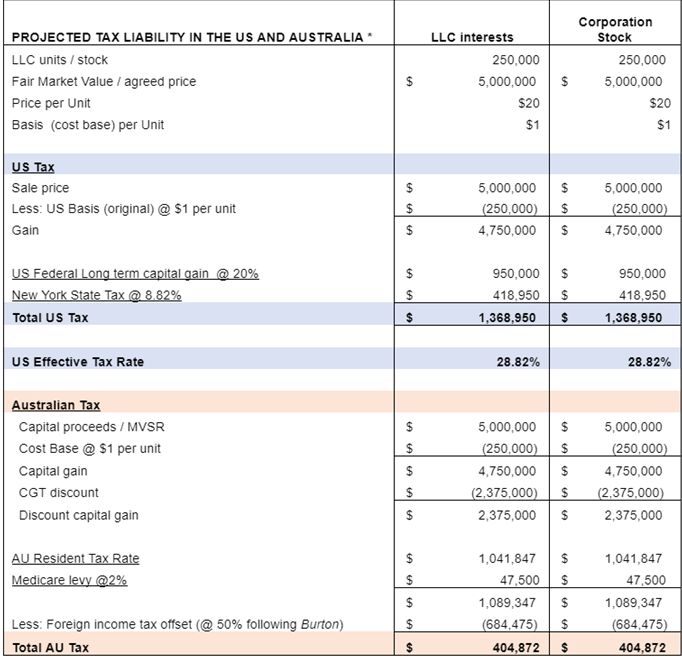

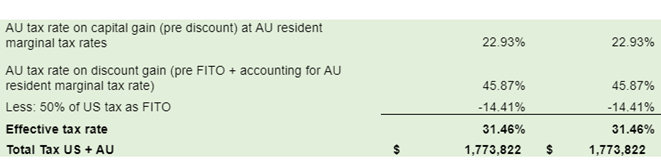

For the LLC member and for the corporate stockholder (who is an Australian resident individual or who receives the gain as beneficiary of an Australian resident discretionary trust), the numbers on a sale could look like this:

- Assumptions:

- AU Tax resident and US nonresident alien

- $ Values are USD and do not account for FX rates

- AU 2020-2021 resident tax rates applied

- Membership interest held by AU resident individual or beneficiary of an AU resident discretionary trust

* This information is of a general nature only and does not take into account other possible structures. It should not be considered a substitute for tax advice specific to your particular circumstances.

For more information, please contact:

Renuka Somers

Head, US-Australia Tax Desk

2025 Australian Federal Budget Summary On Tuesday, March...

In our 13th installment of the Family Office...

2024 Australian Federal Budget Summary On Tuesday 14th...