The 2019 OECD Tax Statistics – how does the US and Australia compare?

The OECD has released its annual Revenue Statistics Report comparing the tax data for all OECD countries .

The OECD Tax Statistics

The 2019 Report indicates that:

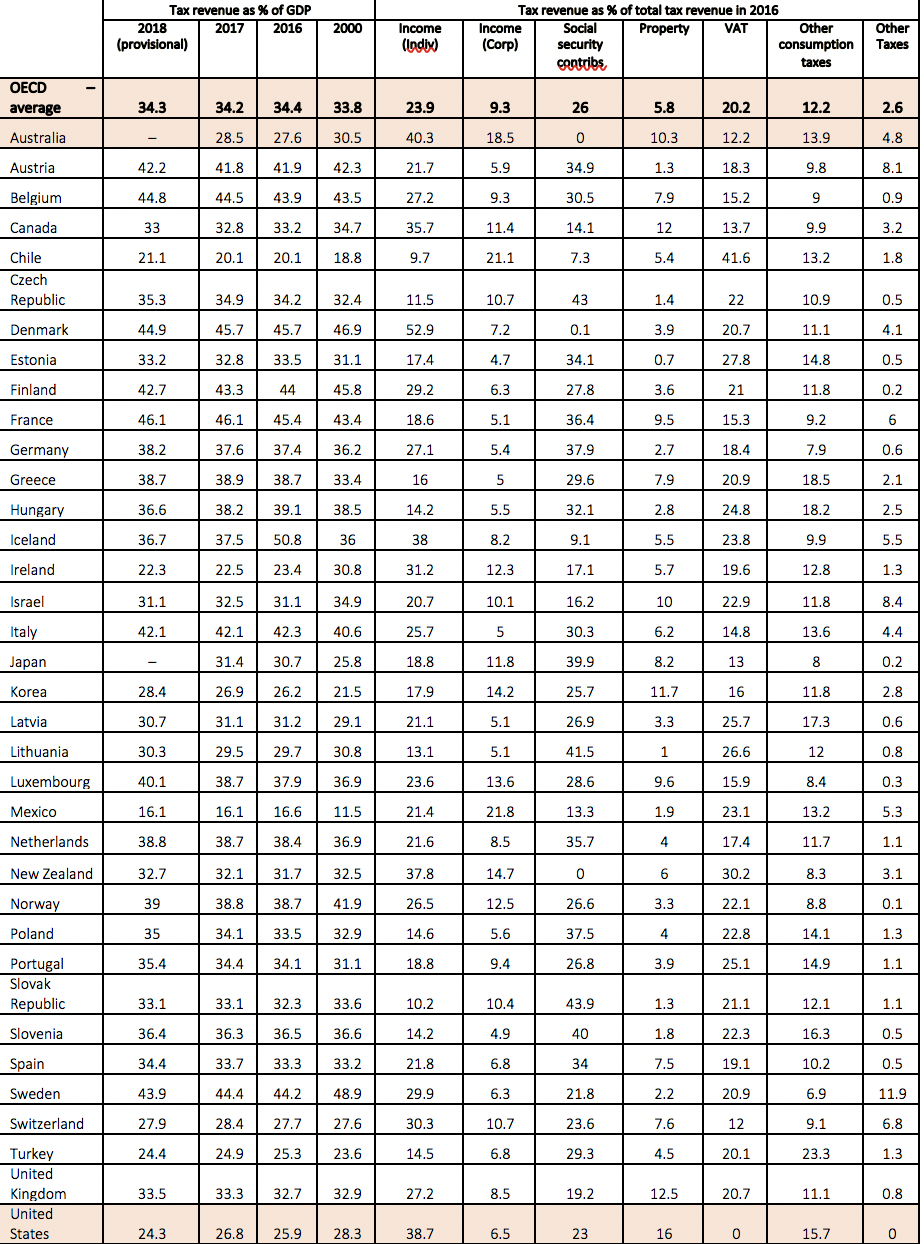

1. the OECD average tax-to-GDP ratio has increased over the past decade, with the average tax-to-GDP ratio being 34.3% in 2018 and country tax-to-GDP ratios varying considerably between countries. France had the highest ratio (46.1%) and Mexico, the lowest (16.1%). The largest increase were seen in Israel (1.4%) and in both Australia (0.9%) and the US (0.9%); and

2. taxes on personal and corporate incomes are the leading revenue sources in 18 OECD countries, with income taxes contributing to over 40% of total revenue in 2017 in both Australia and the US, as well as in Canada, Denmark, Iceland, Ireland, Mexico, New Zealand, Switzerland.

(Refer Annexure A below for a summary of the tax ratios for each OECD country)

The US and Australian Tax Statistics

Of particular interest to us are the US and Australian statistics:

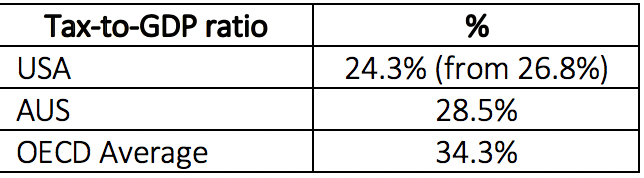

Table 1. US and Australian Tax-to-GDP ratios

1. Tax-to-GDP ratio in Australia increased by 0.9% from 27.6% in 2016 to 28.5% in 2017 (whereas OECD average decreased by 0.2% from 34.4% to 34.2% during that time). Australia had a Tax-to-GDP ratio ranking of 29th place in the 36 OECD countries.

2. In comparison, the US had a tax-to-GDP ratio of 24.3%, ranking it at 32nd place in the 36 OECD countries. The US ratio represented the highest reduction in the ratio (of 2.5%) amongst the OECD countries between 2017 and 2018. The reduction reflects the flow-on effects of tax reform from the US 2017 Tax Cuts and Jobs Act, which lowered the corporate tax rate to 25.8% in 2018 (from 38.9%), reduced income tax rates (with the top rate reducing to 37% from 39.6%), increased in the standard deduction (to $12,000) and doubled the child tax credit (to $2,000 per qualifying child).

3. Interestingly, the tax-to-GDP ratio of both the US and Australia were relatively low, compared to other OECD countries. Both countries had ratios below 30% and ranked in the bottom 1/3rd along with Mexico (16.1%), Chile (20.1%), Ireland (22.5%), Turkey (24.9%), Korea (26.9%), Switzerland (28.4%), and Lithuania (29.5%).

The individual country reports for the US and Australia indicate that the tax structure in each is characterized by:

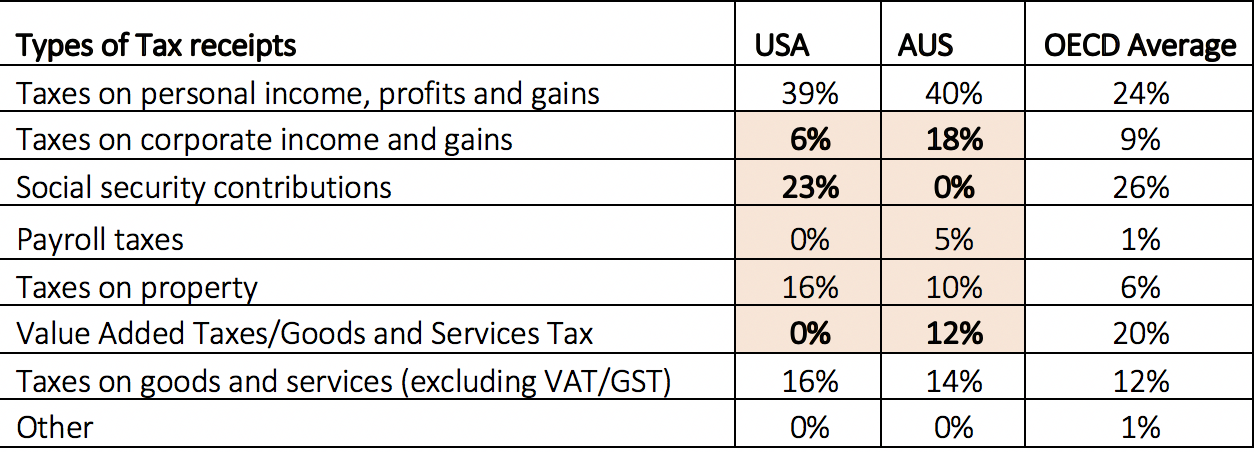

Table 2. US and Australian tax receipts

1. Both countries having substantially high revenue from taxes on personal income, profits and gains, property taxes, and goods & services taxes (excluding VAT/GST).

2. Australia having substantially higher revenue from taxes on corporate income and gains (18%, cf. 6% in the US), payroll taxes (5% cf. 0% in the US), and GST (12%, cf. 0% in the US).

3. Australia having no revenue from social security contributions, whereas the US having 23% of its revenue from such contributions.

4. The United States having the highest share of property tax revenues in 2017 (16.0% of total revenue), largely attributable to repatriation taxes. In contrast, property tax revenue in Australia, was approximately 10% of total tax revenue.

5. Both countries having a federal governance structure. Federal government receipts in 2017 were 80.6% of total revenue in Australia and 44.5% in the US (compared to the OCED average of 53.8%). The State government share of receipts in both countries were similar (18.3% in the US and 16% in Australia), although there was a large disparity at the local government level (14.3% in the US and just 3.4% in Australia).

What opportunities to these Reports present for companies and private clients with interests in both the US and Australia?

These statistics illustrate the tax planning opportunities that the disparities in tax receipts represent. For example, both countries have high personal taxes, whereas there is a significant variation at the corporate level and on payroll taxes, thus representing potential opportunities for business structuring in the US. The variations in taxes on social security contributions and property (with the US being higher) also represent opportunities for structuring retirement contributions and holding property in each jurisdiction.

For more information, contact:

Renuka Somers

Senior Tax Advisor

U.S. Australia Tax Desk

ANNEXURE A. Summary of key tax revenue ratios in the OECD

2025 Australian Federal Budget Summary On Tuesday, March...

In our 13th installment of the Family Office...

2024 Australian Federal Budget Summary On Tuesday 14th...