The U.S.- Australia Estate Tax Treaty Explained

Australia no longer imposes any estate or inheritance taxes (death duties having been abolished in 1979).

The U.S. imposes Federal gift and estate taxes on “U.S. persons” (U.S. citizens and “green card” holders) regardless of where they live. So, if you are a U.S. citizen or green card holder, the gifts you make during your lifetime, and on your death, your estate, are subject to tax in the U.S. if the collective value of the gift(s) or the estate exceeds the exclusion threshold. In 2020, the applicable exclusion amount is US $11.58 million (individual), or US $23.16 million (married spouses). These rates are set to decrease in 2026 to the 2017 rates of US $5.49 million (single) and US $10.98 million (married spouses), indexed for inflation. In addition, estate, gift, and inheritance taxes may also be imposed by the individual States, depending on the location of the property or the deceased’s residency or domicile.

For a non-resident alien, the U.S. Federal estate tax exclusion threshold is presently just US $60,000 (see our blog What are the U.S. Estate Tax Implications for Non-Resident Aliens Holding U.S. Assets? ).

The U.S. and Australia entered into a bilateral estate tax treaty in 1953. Whilst the purpose of the treaty initially was to establish the framework for the imposition of estate taxes by each country, its main purpose now is to:

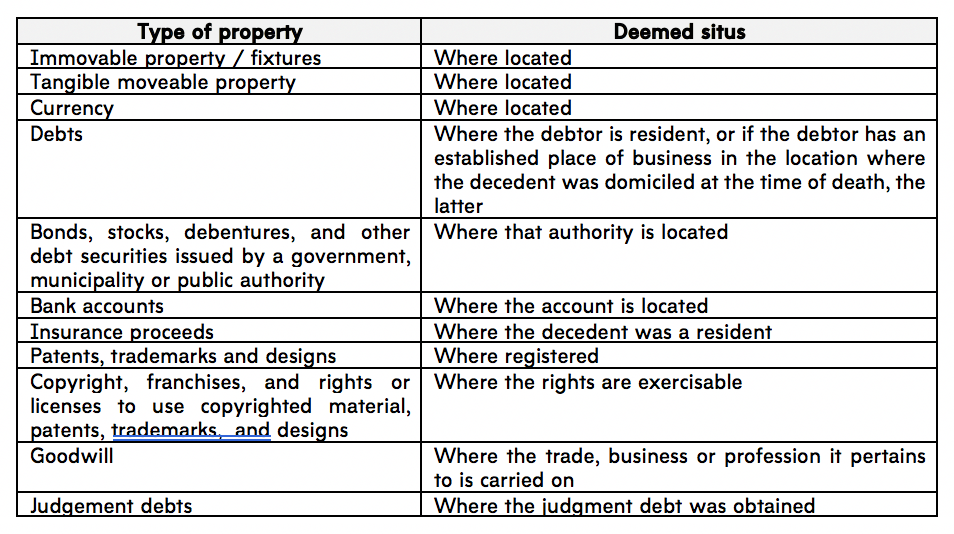

1. Stipulate, in Article III of the treaty, the taxing rights of each jurisdiction based on the location of the decedent’s assets. In summary, these are:

2. Extend, under Article IV of the treaty, the estate tax threshold to Australians who are non-resident aliens of the U.S., the same threshold that would have applied had they been domiciled in the U.S., excluding the value of property located outside of the U.S. Therefore, based on the treaty, the estate tax exclusion for an Australian resident (who is a not a citizen or resident of the U.S.) who holds relevant assets in the U.S. will be extended from US $60,000 to US $11.58 million (at present rates).

Our whitepaper International Estate Planning for U.S.-Australia cross-border clients provides an in-depth analysis of international estate planning issues.

If you have any questions, please contact:

Renuka Somers

Senior Tax Advisor

U.S. Australia Tax Desk

2025 Australian Federal Budget Summary On Tuesday, March...

In our 13th installment of the Family Office...

2024 Australian Federal Budget Summary On Tuesday 14th...