Australian Federal Budget Summary 2023-24

Australian Federal Budget Summary 2023-24

On Tuesday, 9th of May, Treasurer Jim Chalmers delivered a budget surplus of $4.2 billion while at the same time predicting far less enthusiasm in the coming years. Cost-of-living relief was high on the priority list, and there were some historic investments in both Medicare, PBS, NDIS and the care economy broadly.

Summary:

Taxation

• Personal tax rates for 2023-2024 unchanged (Noting the expiry of Low & Middle Income Tax Offset at 30 June 2022).

• Stage 3 personal tax for 2024-2025 unchanged

• Foreign Resident’s tax rate for 2023-2024 unchanged

• Medicare levy low-income thresholds for 2022-23 will increase

Superannuation

• Non-arm’s length income (NALI)

• Super account balances above $3 million

• Super guarantee (SG)- Pay day

• Pension drawdowns – removal of SO% reduction in minimum from 1st July 2023 (FY24)

Cost of living relief

• Cheaper Childcare

• Changes to the Paid Parental Leave scheme

• Cheaper medicine

• Fee-Free TAFE and funding for Higher Education

• Energy price relief

• Increase to base rate of social security

• Increased rent assistance

• Improving Aged Care Support, home care, and funding model

Business

• Small businesses instant asset write-off threshold changes to maximum $20,000

• Small Business Energy Incentive

• Small Business lodgement penalty amnesty program

• PA VG and GST instalment uplift factor

• Part IVA: scope of the general anti-avoidance rules

• FBT rules for electric vehicles (EVs): the eligibility of plug-in hybrid electric cars

Note: These changes are proposals only and may or may not be made law

Full Summary

Taxation

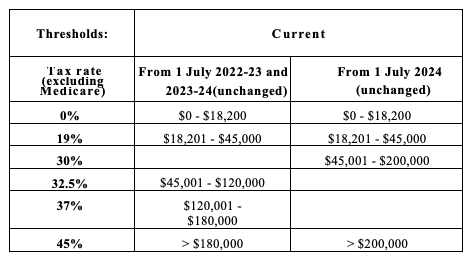

Personal tax rates unchanged for 2023-2024

The personal income tax cuts proposed in the FY2022 budget remain the same going forward

Low-income tax offset for 2023-24 (unchanged)

Low and middle-income taxpayers remain entitled to the low income tax offset (LITO). No changes were made to the LITO in the 2023-24 Budget. The LITO will continue to apply for the 2023-24 income year and beyond.

Low & Middle Income tax Offset (LMITO)

The temporary LMITO was introduced in the 2018-19 budget, extended during the pandemic, and then increased by the Morrison government (and supported by the then opposition) during its pre-election March 2022 budget for a single year.

Neither Labor nor the Coalition had ever planned for it to be retained for 2022-23 or beyond and as such the offset has expired.

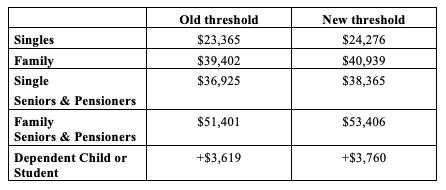

Increase to Medicare Levy low-income thresholds for 2022·23

Superannuation

Non-Arm’s Length Income Changes

The government will amend the non-arm’s length income (NALI) provisions which apply to expenditure incurred by superannuation funds by:

• limiting income of self-managed superannuation funds (SIVISF) and small Australian Prudential Regulation Authority (APRA) regulated funds that are taxable as NALI to twice the level of a general expense. Additionally, fund income taxable as NALI will exclude contributions

• exempting large APRA regulated funds from the NALI provisions for both general and specific expenses of the fund

• exempting expenditure that occurred prior to the 2018-19 income year.

Superannuation Guarantee (SG) and investing in SG compliance, increasing the payment frequency to align with the pay cycle.

From l July 2026, employers will be required to pay their employees’ SG entitlements on the same day that they pay salary and wages. Currently, employers are only required to pay their employees ‘ SG on a quarterly basis. By increasing the payment frequency of superannuation to align with the payment of salary and wages, this measure will both ensure employees have greater visibility over whether their entitlements have been paid and better enable the ATO to recover unpaid superannuation. Increased frequency of payment will also support better retirement outcomes.

Better Targeted Superannuation Concessions

As announced in March, the Government will reduce the tax concessions available to individuals with a total superannuation balance exceeding $3 million from l July 2025.

Individuals with a total superannuation balance of less than $3 million will be fine.

It will bring the headline tax rate to 30 percent, up from 15 percent, for earnings corresponding to the proportion of an individual’s total superannuation balance that is greater than $3 million. Earnings relating to assets below the $3 million threshold will continue to be taxed at 15 percent, or zero percent if held in a retirement pension account.

Cost of living relief – Families, Social Security and Aged Care

Cheaper childcare

Commences from July this year, the Government is delivering Cheaper Child Care, cutting the cost of care for around 1.2 million families. It will make it easier for parents and carers, particularly women, to participate in the workforce and means more children can access the benefits of early education.

• Lifting the maximum CCS rate to 90% for families earning $80,000 or less

• Increasing CCS rates for around 96% of families with a child in care earning under $530,000

• Investing $33.? million to increase subsidized ECEC to a minimum of 36 hours per fortnight for families with First Nations children

Changes to the Paid Parental Leave Scheme

The October Budget committed $531.6 million to deliver a more flexible and generous Paid Parental Leave scheme. From l July this year, Parental Leave Pay and Dad and Partner Pay will combine into a single 20-week payment. A new family income test of $350,000 per annum will see nearly 3,000 additional parents become eligible for the entitlement each year. The Government has committed to increase Paid Parental Leave to 26 weeks by 2026.

Cheaper medicine

The Government will support more than 300 Pharmaceutical Benefits Scheme medicines to be dispensed in greater amounts, phased in from l September 2023. Some patients will be able to get 2 months ‘ worth of the medicine they need for a stable, chronic health condition, cutting the number of visits to a pharmacy and GP each year and saving $1.6 billion in out-of-pocket costs over 4 years.

General patients will be able to save up to $180 a year per medicine if prescribed for 60 days, and concession card holders up to $43.80 a year per medicine.

For at least 6 million Australians this will cut the cost of medicines by up to half and will come on top of the $12.50 decrease in the PBS co-payment for general scripts that came in on l January 2023.

Fee- Free TAFEs and Higher Education

The Government is funding 300,000 TAFE and vocational education training places to become fee-free.

The Government is delivering the second tranche of its commitment for 20,000 additional supported university places in 2023 and 2024.

• Additional funding of $18.7m over 4 years from 2023-24 (and $4.7m per year ongoing)

to extend and expand existing higher education student support programs.

Energy Price Relief Plan

The Government will allocate $1.5 billion over two years from 2023-24 to establish the Energy Bill Relief fund. This fund will support targeted energy bill relief to eligible households and small business customers, which includes pensioners, Commonwealth Seniors Health Card holders, family Tax Benefit A and B recipients, and small business customers of electricity retailers.

Increase to the base rate of social security

The Government will increase support for people receiving working age payments including the JobSeeker Payment. This measure will:

• Increase the base rate of working age and student payments by $40 per fortnight. This increase applies to the JobSeeker Payment, Youth Allowance, Parenting Payment (Partnered), Austudy, ABSTUDY, Disability Support Pension (Youth), and Special Benefit. It will commence on 20 September 2023

• Extend eligibility for the existing higher single JobSeeker Payment rate for recipients

aged 60 years and over, to recipients aged 55 years and over who are on the payment for 9 or more continuous months.

• The increased support for recipients aged 55 years and over, the majority of whom are women, acknowledges the additional challenges older Australians face in re entering the workforce, such as age discrimination or poor health.

Increased Support for Commonwealth Rent Assistance Recipients

The Government will increase the maximum rates of the Commonwealth Rent Assistance (CRA) allowances by 15 percent to help address rental affordability challenges for CRA recipients.

Improving Aged Care Support, home care, and funding model

The Government will introduce a new hoteling supplement of $10.80 per resident per day by separating out the existing hoteling component of the Australian National Aged Care Classification (AN-ACC) price (the $10 Basic Daily Fee Supplement) starting l July 2023. The Government will also adjust the care minute allocations within the AN-ACC funding model from l October 2023 to better align care minutes with resident needs. The Government will provide:

• $487.0 million over 4 years from 2023-24 (and $133.6 million ongoing) to extend, and make ongoing, the Disability Support for Older Australians Program.

• $41.3 million over 4 years from 2023-24 (including $11.9 million in capital funding from 2022-23) to build a new place assignment system, allowing older Australians to select their residential aged care provider.

• additional funding to improve the in-home aged care system, including $166.8 million in 2023-24 to release an additional 9,500 Home Care Packages.

Business

$20,000 Instant Asset Write-off

Small businesses with annual turnover of less than $10m will be able to immediately deduct eligible assets costing less than $20,000 from l July 2023 until 30 June 2024. The $20,000 threshold applies on a per asset basis, so small business can instantly write off multiple assets (there is no cap on the total amount that can be instantly written off). Assets valued at

$20,000 or more can continue to be placed into the small business simplified depreciation pool and depreciated at 15 percent in the first income year and 30 percent each income year thereafter.

Small Business Energy Incentive

To help small and medium businesses electrify and save on their energy bills, this incentive will provide tax relief and support to businesses making investments like electrifying their heating and cooling systems, installing batteries, and upgrading to high-efficiency electrical goods. Businesses with annual turnover of less than $50m will have access to a bonus 20 percent tax deduction for eligible assets supporting electrification and more efficient use of energy from l July 2023 until 30 June 2024. Up to $100,000 of total expenditure will be eligible for the incentive, with the maximum bonus tax deduction being $20,000 per business.

Small Business lodgement penalty amnesty program

A failure-to-lodge penalty (FTLP) amnesty for small business with aggregate turnover of less than $10M. For outstanding tax statements that were originally due in the period l December 2019 to 29 February 2022. The amnesty will remit FTLPs if the outstanding statements are lodged in the period l June 2023 to 31 December 2023.

Improving small business cash flow – PAVG and GST

The Government is providing eligible small businesses with cashflow relief by halving the increase in their quarterly tax instalments for GST (businesses with turnovers up to $10M) and income tax (businesses with turnovers up to $50M) in 2023-24. Instalments will only increase by 6 percent instead of 12 percent, allowing small businesses to manage cash flow given the current economic conditions.

Scope of Pt IV A to expand to catch two additional types of schemes

The Government will expand the scope of the general anti-avoidance provisions in Pt IVA of the ITAA 1936 so that they can apply to:

• Schemes that reduce tax paid in Australia by accessing a lower withholding tax rate on income paid to foreign residents. Part IVA already applies to schemes that produce a tax benefit by not having any withholding tax liability in respect of an amount paid to a foreign resident

• Schemes that achieve an Australian income tax benefit, even where the dominant purpose was to reduce foreign income tax.

This measure will apply to income years commencing on or after l July 20 24, regardless of whether the scheme was entered into before that date.

FBT rules for Electric Vehicles – Rules for plug-in hybrids to sunset

The Budget papers state that the Government will sunset the eligibility of plug-in hybrid electric cars from the FBT exemption for eligible electric cars. This change will apply from l April 2025. Arrangements involving plug-in hybrid electric cars entered into between l July 2022 and 31 March 2025 remain eligible for the Electric Car Discount.

– Liza Janakievski, Managing Director + Head of Asset Management, (Giles Wade Private Wealth)

2025 Australian Federal Budget Summary On Tuesday, March...

In our 13th installment of the Family Office...

2024 Australian Federal Budget Summary On Tuesday 14th...